2. The financial service of the enterprise, its structure and relationship with others

divisions of the enterprise

Financial service – an independent structural unit that performs certain functions in the enterprise management system (Fig. 2.4). Typically, this unit is the finance department. Its structure and number depends on the organizational and legal form of the enterprise, the nature of financial activities, production volume, the number of employees in the enterprise.

Rice. 2.4. The purpose and objectives of the financial service

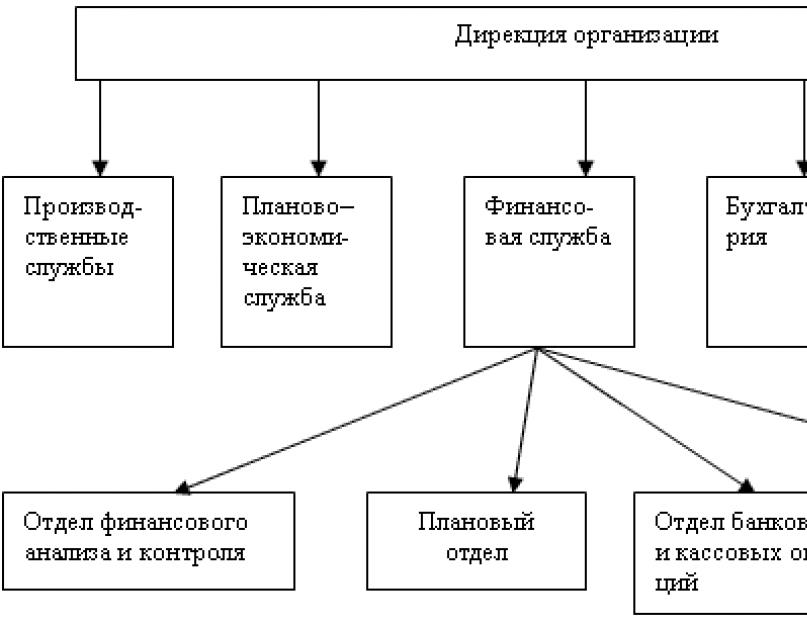

The financial service performs numerous functions. The main ones are financial planning, financial analysis, financial control and financial management. The functions of the financial service are built in full accordance with the content of financial work in enterprises (Fig. 2.5).

Rice. 2.5. Sample Structure financial services

The financial service is part of a single business management mechanism, and therefore it is closely related to other services of the enterprise, and therefore it is closely related to other services of the enterprise.

So, as a result of close contacts with the accounting department, the financial service is provided with production plans, lists of creditors and debtors, documents on the payment of salaries to employees, amounts Money on his accounts, and the amount of future expenses. In turn, the financial service, processing this information, analyzing it, gives a qualified assessment of the solvency of the enterprise, the liquidity of its assets, creditworthiness, draws up a payment calendar, prepares analytical reports on other parameters of the financial condition of the enterprise and acquaints the accounting department with financial plans and analytical reports on their implementation. , which in its daily activities is guided by this information.

From the marketing department, the financial service receives plans for the sale of products and uses it in income planning and operational financial plans. To conduct a successful marketing campaign, the financial service justifies selling prices, approves a system of concessions in the price of the contract, analyzes sales and marketing costs, carries out a comparative assessment of the competitiveness of the company's products, optimizes its profitability, thus creating conditions for concluding large transactions (Fig. 2.6) .

The financial service has the right to demand from all services of the enterprise the actions necessary for the qualitative organization of financial actions and financial flows. In its competence are also such important characteristics enterprise activities like his image, business reputation.

Rice. 2.6. The relationship of the financial service of the organization with other departments

Like any management system, financial management consists of two subsystems: the object of management and the subject of management.

Rice. 2.7. System financial management In the organisation

The object of management in financial management is the cash flow of an economic entity, which is a flow of cash receipts and payments. Certain sources must correspond to each direction of spending money funds: in an enterprise, sources can include equity and liabilities that are invested in production and take the form of assets. In general, the constant process of cash flow is shown in Fig. 2.7.

The process of cash flow management largely consists in forecasting the cash flow for the long term and assessing its impact on financial condition company.

The subject of management is the financial service, which develops and implements the strategy and tactics of financial management in order to increase the liquidity and solvency of the enterprise through the receipt and effective use of profits.

The specific structure of the financial service largely depends on the organizational and legal form of the enterprise, its size, the range of financial relations, the volume of financial flows, the type of activity and tasks set by the company's management. Therefore, the financial service can be represented by various formations (Fig. 2.8).

Rice. 2.8. Types of financial services depending on the size of the enterprise

The financial department of an enterprise usually consists of several bureaus responsible for separate directions financial work: planning bureau, banking operations bureau, cash operations bureau, settlement bureau. Special groups are created within each bureau. The functions of each group are determined as a result of detailing the functions of the bureau.

The financial management of the enterprise combines the financial department, the planning and economic department, the accounting department, the marketing department and other services of the enterprise.

These services report to the Vice President for Finance (Fig. 2.9).

Rice. 2.9. Organizational structure organization management

The concentration in the hands of one directorate of the main enterprise management services significantly increases the possibility of regulatory influence on financial relations and financial flows. In this case, the financial service not only successfully captures the quantitative parameters of the enterprise, but also, thanks to direct participation in the development of the financial strategy and tactics of the enterprise, largely determines their quality.

When determining the content of the work of the financial directorate ( financial manager) it is important to note that it either represents a part of the work of the top management of the enterprise, or is associated with the provision of analytical information to it, with which it is possible to make decisions in the field of finance.

The Directorate as a whole and each of its divisions operate on the basis of the Regulations on the Financial Directorate, approved by the management of the enterprise. It clearly reflects the general aspects of the organization and structure of the financial service, defines specific tasks and functions, relationships with other divisions and services of the economic entity; rights and responsibilities of the management. The tasks facing the financial directorate and its divisions cover all areas of the enterprise.

Financial managers play an important role in managing the financial activities of an enterprise.

In his work, the financial manager is based on the current legislation in the tax, currency, financial and credit areas, proceeds from an assessment of the economic situation in the country and global financial markets. He is subordinate to two functional manager- Comptroller and Treasurer There are no clear distinctions in the work of the controller and the treasurer, their job responsibilities in different companies differ depending on the policy pursued by them, and personal qualities(Fig. 2.10).

Rice. 2.10. Functions of the controller and treasurer in the financial activities of the organization

The functions of the controller are primarily internal in nature. They consist in maintaining accounting records, tracking document flow and monitoring the financial results of activities for the past and current economic activity. The controller is, in fact, the chief accountant of the company and the management entrusts him with the preparation of financial reports, tax returns, and the annual report.

The activities of the treasurer are aimed at solving global issues to ensure financial stability companies. The treasurer manages the enterprise's capital entrusted to him, that is, he forms its optimal structure, evaluates capital costs, manages cash flow, attracts long-term and short-term loans, and organizes settlements with buyers.

The treasurer concentrates his efforts on maintaining the liquidity of the enterprise, receiving cash from obligations and increasing funds to achieve the company's goal. While the controller focuses on profitability, the treasurer emphasizes cash flow by managing the company's receivables and payments. By constantly dealing with these issues, the treasurer can see the signs of bankruptcy in time and warn him.

The financial manager is usually employed as employee under a contract that strictly defines his functional duties, the procedure and amount of remuneration. In addition to the salary, the financial manager, who belongs to the highest management apparatus, can receive remuneration in the form of a percentage of net profit based on the results of the enterprise's activities. Its size is determined supreme body management economic entity: meeting of shareholders, meeting of founders, board of the enterprise. In some countries (USA, Japan), chief financial managers own a stake in the company.

The formation of the financial department at the enterprise is a responsible task. The functions of the financial department are constantly expanding and being formed based on the tasks, the solution of which is the responsibility of the head of the financial department.

Functions of the financial service:

- Financial controlling is one of the main tasks of the financial service, which consists in the formation of plans and control over their execution. The performance of this function is associated not only with accounting and analysis, but also with control over the execution of business processes of the enterprise.

Figure 1. Controlling the execution of the cash flow budget using an example software product"WA: Financier".

- Treasury Department. Cash management of the company, the formation of a payment calendar, control of the status of mutual settlements - all these are functions of the treasury and it is impossible to underestimate their importance.

- Organization and maintenance of accounting and tax accounting. This function does not require much explanation. The only thing I would like to focus on is the delimitation of the functions of the Chief Accountant and the Financial Director (Head of the Financial Department). The responsibility of the chief accountant is to maintain a regulated and tax accounting in accordance with the requirements of the law, timely formation of accounting and tax reporting, reflection of the facts of the company's economic activity on registers accounting. The duties of the head of the financial department are to plan the activities of the company, its financial results, including in the context of constantly changing legislation. The function of tax planning is the direct responsibility of the financial director of the company. The subordination structure of the Chief Accountant is also a topic for a separate discussion. On the one side Chief Accountant belongs to the area of responsibility of the financial director and must report to him, on the other hand, in accordance with the law "on accounting", the chief accountant reports directly to the General Director of the organization. The easiest way out in this situation is the dual subordination of the chief accountant.

It should be understood that in a particular company, the scheme of work of the financial department may not limit the tasks facing the financial director in the process of organizing the department.

After the responsibilities of the financial department are defined, it is possible to start forming its structure.

The work of the financial service can be organized as follows:

Figure 2. The structure of the financial service.

At the same time, the subdivisions "Contractual Department" and "IT Department" are not part of the FEO, but are strategically subordinate to the Financial Director.

The simplest thing is to allocate a separate service to implement each function.

But no one bothers to split the function into several services or, conversely, combine several functions into one service.

Having determined the structure and tasks of the financial department, it is necessary to start developing internal regulations.

Regulations for the work of the financial department

What do financial services regulations include?

Regulation of the financial department is a set of provisions, rules, instructions governing business processes owned by the financial director, and as basic ones (budgeting, accounting, fundraising, making payments; regulated accordingly by budgetary, accounting, credit policies, the procedure for making payments, preparation of financial statements), and directly related to the management of personnel of the financial service of the enterprise. The latter are often referred to as HR processes.

In the process of developing, coordinating and approving documents regulating these processes, many issues related to the number of employees of the financial service, the requirements for their qualifications, and the wage fund are removed. When the requirements for functional duties employees on the part of the company's management, the regulatory documents approved earlier will minimize potential conflicts, change the staffing level and revise wages.

Figure 3. The approval process on the example of the software product "WA: Financier".

The set of tasks of the financial department, its regulations and structure form the basis for the formation of the final document - the Regulations on the financial service of the enterprise.

This provision is an internal regulatory document, which has the following structure:

1. Organizational and functional structure of the financial service. Typically, the organizational structure is an organizational chart with the allocation of departments and a description of their functions. For the purposes of HR planning, it is useful to display information on the number of staff units(existing and planned).

2. Structural and headcount financial service. As a rule, this information is formed in the form of a table with the obligatory indication of the names of departments, positions, the number of active and vacant staff positions.

3. The main goals and objectives of the financial service. This section of the regulation describes the goals formulated taking into account the company's development strategy, and the tasks that need to be solved to achieve them. Tasks are defined for each department.

4. Matrix of functions. This is a table in which the functions of the financial service are located vertically, and organizational units are located horizontally, that is, managers and key employees service departments s. At the intersection of the lines and the graph, a mark is made (who is responsible for what). The function matrix gives an idea of the possible workload of departments and allows you to optimally group functions by department.

5. The order of interaction of employees of the financial service. Usually, the internal order of interaction is distinguished - between individual employees and (or) structural divisions of the company and external - with individuals (for example, especially large clients) or state (commercial) organizations. The order of interaction is developed taking into account the organizational structure of the company as a whole, the functions and tasks of its other divisions, established principles and traditions.

Figure 4. The order of interaction of employees on the example of the software product "WA: Financier".

6. Procedure for resolving conflict situations. This section details the procedure for filing an appeal or expressing disagreement along the chain “general director - financial director - head of the financial and economic department - ordinary employee”. This applies to any questions and proposals (the task received, the decision being made, disproportionate compensation, encouragement or punishment), including innovative ones that may arise both for the employee and his immediate supervisor.

7. A system of indicators to evaluate the work of the financial director and the financial service. This section includes lists and descriptions of indicators, upon fulfillment of which the work of the financial director and his subordinates is recognized as successful. Indicators should be specific and measurable.

8. Final provisions. This part establishes the procedure for agreeing and approving the Regulations, its validity period, the procedure for making changes, familiarizing employees with the Regulations and the procedure for storing it.

If the head of the financial service is the financial director, then his activities are regulated by the job description of the financial director. If the planning and financial department is separated into a separate unit, then when developing job description the head of the financial department must apply general rules formation of job descriptions.

A detailed job description usually includes the following items:

1. General provisions- description of the document, position, who appoints the employee to this position, etc.

2. Qualification requirements. The requirements for the level of education of a specialist in this position are formulated, and a set of skills and abilities necessary to perform job duties is described.

3. Job responsibilities. The more detailed this section is filled out, the less questions the specialist will then have about the need to perform certain tasks. Therefore, this section should be the most complete summary of all possible tasks performed by a specialist.

4. Criteria for the success of the performance of labor duties. The section is quite difficult to fill in, since it is not always possible to formulate these criteria. It makes sense to describe only those criteria, the fulfillment of which can be controlled.

5. Rights of a specialist. The duties of the company to the specialist are described. This is a timely payment. wages, organization of the workplace and technological infrastructure, compliance with sanitary standards, etc.

6. Rights and obligations of the head. This paragraph complements the previous one. It contains an explanation of the duties and powers of the immediate supervisor of the specialist.

7. Responsibility of a specialist. A paragraph that describes what the employee is directly responsible for and contains information about possible penalties for failure to perform official duties.

It should be noted that the effective operation of the financial department is impossible without a high-quality information system.

More and more organizations are choosing a solution based on the 1C platform - "WA: FINANCIST", which is a line of software products for automating financial management in medium and large businesses.

Modules "WA: FINANCIST":

- Treasury, BDDS

- Budgeting of income and expenses, BBL, etc.

- Accounting and reporting under IFRS

- Management accounting according to corporate standards

- Contract management: from approval to execution

Figure 5. Formation of ODDS by direct and indirect methods on the example of the software product "WA: Financier".

With the use of "WA: FINANCIST" financial departments of enterprises effectively solve the following tasks:

- Forecasting the financial condition of the enterprise and modeling economic indicators business, determination of planned results.

- Convenient and error-free planning / control of income, expenses and cash flows of the company.

- Optimizing the use of money, increasing financial efficiency and business sustainability.

- Increasing the liquidity and profitability of the business, including by minimizing the use of borrowed funds.

- Improving quality and validity management decisions and business transparency in general.

- Timeliness and reliability of financial statements in accordance with international or corporate standards.

- Full order in working with contracts: storage, approval, and comprehensive control.

- Increasing financial discipline in the company as a whole and the degree of personal responsibility of employees.

- Reducing labor costs, increasing convenience and minimizing the mistakes of financiers in their daily work.

See the following sections for details.

One can hardly argue with the fact that the creation of a financial department of a commercial structure is a very responsible task, because its functionality is periodically expanded. As a rule, its elements are formed on the basis of those tasks, the solution of which should be dealt with directly. Which of them are relevant today? What are the responsibilities of a leader? What information does the job description contain? If you wish, you can find the answer to these and other questions in the article.

The functionality of the financial service of the enterprise

Initially, it should be noted that the tasks that are formed on the basis of the functions listed below should be solved directly by the head of the financial and economic department, so he must know the functionality without fail. What does the financial service do?

Firstly, it is controlling in the financial sector, which consists in creating certain plans and monitoring their quality execution. It is important to note that it is closely interconnected not only with analysis and accounting, but also with the control of the competent execution of various business tasks of a commercial structure.

Additional functions

The second function of the financial service of any enterprise is the treasury, which implies the management of the enterprise's money, the creation and subsequent maintenance of a payment calendar, as well as control directly over the state of various levels of mutual settlements. By the way, it is impossible to overestimate the functionality of the Treasury. The final function is the organized formation and further maintenance of accounting.

Job description of the head of the financial department of the enterprise

Before proceeding to consider the job description of the head of the financial department of a commercial structure, one nuance should be clarified. If the head of the financial department of the company is directly the financial director, then his activities can be regulated by means of an appropriate document. If the financial department is an independent unit, then the instruction ( position) head of the financial and economic department is developed taking into account the application general algorithm creation of such business papers.

Algorithm: general provisions, requirements and responsibilities

The general algorithm for generating job descriptions usually includes the following elements:

- General provisions - imply a description of the document, an indication of the position for which the employee is accepted. IN this case appropriate

- Current qualification requirements. Among them, the level of education of the employee, a set of skills and abilities that are needed to perform job duties.

- Job description of the head of the financial and economic department also includes job responsibilities. It is important to note that this section must be completed in as much detail as possible. This should be done so that the employee has fewer questions about certain tasks that the specialist must perform.

Success criteria and employee rights

In addition to the above items, it includes the following components:

- Criteria that determine success in terms of performance of official duties. It should be noted that this section is quite complicated in relation to filling, because it is far from always possible to form these criteria. In addition, it is important to consider only those criteria, the implementation of which is fully subject to control.

- Also job description of the head of the financial department contains information about the rights of a specialist. In this section, the duties of the enterprise to the employee are presented directly. Among them, as a rule, are timely salaries, high-quality organization of the workplace and, of course, infrastructure in terms of technology, as well as absolute compliance with standards in terms of sanitation.

Powers of the head and responsibility of the employee

Additional elements of a standard job description:

- The section arguing the rights and duties of the head, in its structure, is some addition to the previous one. It contains explanations about the powers of the head of this specialist.

- The responsibility of the employee implies a description of what the specialist is responsible for, and contains information about possible penalties in case official duties head of financial department.

It should be noted that the implementation efficient operation of the financial department is impossible in the case of a poor-quality system for providing information!

General provisions. Detailed description

In accordance with the general provisions of the job description, he must have a higher professional (engineering and economic or standard economic) education, as well as work experience in the specialty (organization of the financial activities of the structure) for at least five years. In addition, an employee of this category must know:

- Legal acts in terms of regulations and legislation that regulate the activities of the structure regarding the economy and production.

- Information of a normative and methodological nature that directly relates to financial transactions companies.

- Prospects for the development of the structure.

- The current state, as well as development prospects in relation to the markets for the products or services provided, as well as financial markets.

- Technologies affecting production processes.

- Competent organization of financial activities in the company.

What does a finance manager need to know?

In addition to the points above, you should know:

- The current procedure for the formation of plans in relation to the finances of the enterprise, as well as forecasts in relation to the sale of products or services provided.

- A set of methods and levers that provide direct management of financial flows.

- The current procedure regarding financing from the state budget, lending both in the short and long term, attracting investments, as well as using own funds and acquiring various types of securities (stocks, bonds).

- The current procedure for the distribution of financial resources, as well as identifying the effectiveness of investments.

- Rationing in respect of working capital.

- The current procedure and, accordingly, the forms of financial settlements.

- Legislation in the field of taxation.

- Standards in terms of financial accounting and reporting.

- Economic processes, organization of production operations.

- Accounting.

- Technique for calculation, the basics of working with it.

- Labor law provisions.

- Rules and regulations in terms of labor protection.

Head of Finance Department: Responsibilities

The job description specifies the following duties of the head of the financial department of the enterprise:

- Organization of management in relation to the movement of the company's financial resources and competent regulation of relationships in the field of finance, which, as a rule, arise between business entities in market conditions. This must be done in order to maximize the effective use of various components. resource potential enterprises during the production process, as well as the implementation of the manufactured product or services provided to obtain the maximum amount as a profit.

- Ensuring the development of the financial strategy of the structure, as well as its financial stability.

- Guidance in relation to the development of projects of both current and long-term financial plans, as well as forecast balances and budgets of cash resources.

Tasks of the head of the financial service

What else is he obligated to do? Its activities typically include the following:

- Ensuring that financial values that have already been approved are communicated to the relevant departments of the company.

- Active participation in the development of projects in relation to the planning of the sale of manufactured products or services, capital investments, research and innovative developments in scientific field, planning about the cost of the product, as well as the profitability of the production itself.

- Direct participation in the calculation of profits and, of course, income tax.

- Determination of sources for financing the company's activities in production and economic terms (budget financing, lending both in the short and long term, the formation and purchase of securities, financing in relation to leasing operations, raising borrowed funds, efficient use of own financial resources).

What else does the head of the finance department do?

In addition to the duties listed above, he is obliged to carry out the following items of instructions:

- Conducting research and detailed analysis of financial markets, assessing possible risks in relation to managing financial flows, developing proposals to minimize these risks.

- Implementation of the investment policy, as well as competent asset management of the structure (determination of their optimal composition, preparation of proposals for the replacement or liquidation of active funds), analysis and formation of an appropriate assessment that determines the effectiveness of financial investments.

- Organization of the development of working capital norms, as well as measures to significantly accelerate their turnover.

- Ensuring the timely receipt of income, processing banking and financial transactions within a certain timeframe, paying contractors and suppliers, repaying various types of loans, paying bank interest, salaries to employees of the enterprise, transferring tax payments to the budgets of the federal, regional and local levels, as well as to off-budget state funds of a social nature.

Additional Responsibilities of the Chief Financial Officer

The following items are final in the list of duties of the head of the financial service:

- Qualitative analysis of the economic and economic activities of the structure, participation in the formation of proposals aimed directly at organizing the company's solvency, preventing the creation and exclusion of unusable values of a commodity-material nature, maximizing profitability in relation to production processes, increase in profits from the sale of products, a significant reduction in costs both in terms of production and in relation to the sale of the product, strengthening discipline in relation to finances.

- Monitoring the implementation of financial, implementation, profit and other plans, stopping the production of a product that does not have a market, competent spending in relation to the financial resources of the enterprise and the targeted use of both own and borrowed working capital.

Final chord

Another important duty of the head of the financial service of any commercial structure is to ensure that accounting for the movement of funds of a financial nature and the formation of reports on the results of various financial transactions in accordance with current accounting and reporting standards, as well as the reliability of financial information. In addition, the head of the financial department monitors the correctness of reporting documents, the timeliness of their submission to both external and internal users. And of course, this employee most effectively manages the specialists of the financial service.

The purpose of financial work is to organize the circulation of capital with financial resources and distribute them in an optimal way over different stages of the circulation.

The listed tasks have specific implementation mechanisms, their own rules and techniques, far from the rules and techniques of accounting. Although financial work is regulated by state-level regulations, the financial manager is more free in making management decisions.

Therefore, the following provisions are included in the responsibilities of the financial department:

ѕ drawing up tactical and operational plans for financing;

ѕ calculation and adjustment of the norms of working capital for individual items, elements, types of reserves and costs in general for the organization;

- identification of sources of financing, determination of volumes and sources of investments, formation of reserve funds and financial reserves of the enterprise;

ѕ consideration of prices for products manufactured by the organization, control over the use of funds, funds and reserves, the formation of financial and economic calculations, participation in the preparation of draft contracts, justification of forms of payment.

The financial department in its activities is closely connected with the economic, supply and marketing, technical and production services of the enterprise and, together with other departments, provides:

ѕ with the marketing service and sales department - preparation of planning documentation for deliveries finished products, development of prices, payment terms;

ѕ with the supply service - development of prices and delivery schedules, determination of the optimal order size and stocks, control over stocks of inventory items;

* with department capital construction- development of title lists of construction sites and facilities, plans for financing capital investments by the production services of the enterprise - participation in the development of norms, standards and consumption limits production resources, control over the remains of work in progress;

* with design and technological services - participation in the preparation of plans for research and development work, organization of funding;

ѕ with accounting - checking the correctness of the preparation of estimated and financial estimates, these audits and inventories.

Organization of financial work

Formation of financial work in the organization - in market conditions in the formation correct operation the goal is to fulfill obligations to budgets in a timely manner, own employees at the enterprise, other business entities, the credit system, as well as effective financial management - management.

The organization of financial work at the enterprise involves the optimization of management cash flows that arise in the course of financial and economic activities, maximizing profits and improving the welfare of the owners of the enterprise.

Financial work at the enterprise, as a rule, is allocated to an independent service, its size is determined by the scale of activity and industry characteristics. For example, at large enterprises, in holdings, financial directorates or financial organizations are created as independent structural units. The Head of Finance reports directly to to CEO(director) of the organization and together with him is responsible for the financial condition commercial organization. Usually CFO large enterprise has subordinated several functional financial works, that is, structures (links): cash flow management, financial planning, borrowing and issuing securities, investing, risk management and insurance.

The organization of financial work in a medium-sized enterprise is concentrated in the financial department or is entrusted to a specialist in the field of financial management - a financial manager who is part of the functional economic unit. Financial work can also be performed by financial sectors as part of the planning and financial, financial and marketing, financial and accounting or other divisions of the enterprise. Functional structures for managing financial work in small enterprises, as a rule, are not created. Due to the insignificant volume of organization of financial work at the enterprise, the obligations for its execution are usually assigned to the owner of the enterprise, its director or accountant.

Regardless of the scale of activity, the peculiarities of financial management at the enterprise, such work includes three areas: financial planning, operational work and control and analytical work. In its course, the following main tasks are solved:

* providing the necessary financial resources to replenish production and social development;

ѕ solution of problems to increase profits and increase profitability;

ѕ ensuring the fulfillment of one's own obligations to the budgets, employees of the enterprise (in terms of wages), suppliers, banks, etc.;

* determination of ways of efficient use of property, fixed assets and working capital;

* control investment activity and achieving maximum financial performance;

ѕ organization of control over financial decisions, rational use of financial resources, safety of working capital.

Organization financial management at the enterprise helps the company to survive in a competitive environment, to ensure sustainable financial position, maximizing the "price" of the enterprise, profits, minimizing costs, profitability, growth in production and sales. The enterprise has the right to increase its own income through its core activities and actively stock market(securities market), take part in the activities of other enterprises and organizations, master related areas of activity, use other financial work enterprises where there is no contradiction to the law, all this is necessary for the possibility of increasing the total financial result.

|

APPROVE |

|||||||

|

(Business name, |

|||||||

|

(head of the enterprise |

|||||||

|

organizations, institutions) |

|||||||

|

organizations, institutions) |

|||||||

|

POSITION |

|||||||

|

00.00.0000 |

№ 00 |

(signature) |

(surname, initials) |

||||

|

00.00.0000 |

|||||||

The financial department is an independent structural subdivision of the enterprise and reports directly to the Deputy Director for Economic Affairs.

II. Tasks

Organization of the financial activity of the enterprise, aimed at providing financial resources plan assignments, safety and efficient use of fixed assets and working capital, labor and financial resources of the enterprise, timeliness of payments for obligations to the state budget, suppliers and banking institutions.

III. Structure

1. The structure and staff are approved by the director of the enterprise in accordance with the standard structures of the management apparatus and the norms for the number of specialists and employees, taking into account the volume of work and production features.

2. The department may include divisions (sector, bureau, group) of financial planning, analysis of financial and economic activities, organization of settlements with suppliers, collection, cash transactions, etc.

IV. Functions

1. In the field of financial and credit planning

1.1. Drawing up in due time draft financial plans of the enterprise with all the necessary calculations, taking into account the maximum mobilization of on-farm reserves, the most rational use of fixed and working capital.

1.2. Compilation and submission of loan applications and quarterly cash plans to the higher organization and institutions of banks in a timely manner and participation in their consideration.

1.3. Participation in the preparation of a plan for the sale of products in monetary terms. Determination of the planned amount of balance sheet profit for the year and by quarters and profitability indicators.

1.4. Drawing up, together with the planning and economic department, planned calculations for the formation of economic incentive funds and participation in the preparation of estimates for their spending.

1.5. Determination of the planned amount of depreciation deductions divided into full restoration (renovation) of fixed assets a overhaul.

1.6. Participation in determining the need for own working capital by elements and calculation of working capital standards.

1.7. Drawing up a plan for financing centralized capital investments and a plan for financing the overhaul of fixed assets.

1.8. Drawing up plans for the distribution of balance sheet profit and depreciation.

1.9. Participation in the preparation of plans for financing research work on the basis of the envisaged scope of these works, as well as determining the sources of financing for plans for organizational and technical measures, taking into account the calculations of economic efficiency.

1.10. Planning the average annual cost of fixed production assets and fixed assets exempted from payment for funds.

1.11. Making settlements for filing claims with suppliers and contractors and for transferring export premiums.

1.12. Distribution of quarterly financial indicators by months.

1.13. Participation in the preparation of the VAT plan.

1.14. Bringing the indicators of the approved financial plan and the tasks arising from it, limits, norms and standards of working capital to departments, services, workshops of the enterprise and the implementation of systematic monitoring of their observance and implementation.

1.15. Drawing up operational financial plans for the coming month and for intra-month periods.

1.16. Drawing up operational plans for the sale of products in monetary terms and plans for profit.

1.17. Participation in the preparation of operational schedules of shipment marketable products.

1.18. Implementation of control over the delivery of inventory items in order to prevent the accumulation of excess stocks.

1.19. Ensuring the implementation of financial, credit and cash plans.

2. In the field of financial and operational work

2.1. Ensuring on time:

payments to the state budget - for turnover tax, for production assets and other payments

interest payments on short-term and long-term loans;

contributions from own funds from profits, depreciation and other sources to finance centralized and non-centralized capital investments;

transfers of funds to special accounts (under the production development fund), etc.;

transfer of funds in the order of intradepartmental redistribution of profits; working capital, depreciation deductions, as well as funds for financing research and development, development new technology and other goals provided for in the financial plan;

transfers of funds to centralized funds and reserves of a higher organization;

the issuance of wages to employees of the enterprise and the implementation of other cash transactions;

payment of invoices of suppliers and contractors for shipped material assets, services rendered and work performed in accordance with the concluded agreements;

payment of interest on credit on long-term and short-term bank loans.

2.2. Providing financing for the costs provided for by the plan.

2.3. Arrangement of requested loans in accordance with current rules lending and ensuring the return of loans received in a timely manner.

2.4. Carrying out operations on the accounts of the association and the parent company in banking institutions.

2.5. Presentation to bank institutions issued in in due course payment requests, other settlement documents for shipped products, services rendered and work performed; ensuring timely receipt of documents for the shipment of products, issuing invoices and taking measures to timely receive funds due from buyers.

2.6. Maintaining daily business records:

sales of products, profits from the sale of other financial indicators;

refusals of buyers to accept payment requests for shipped products, services rendered and work performed due to the reasons for refusals and taking appropriate measures on them;

fulfillment of other indicators of the financial plan.

2.7. Drawing up and submission to the management of the enterprise of information and certificates on the progress of the implementation of the main indicators of the financial plan and on the financial condition.

2.8. Drawing up and timely submission of the parent organization, financial authorities and institutions of banks of the established operational financial statements.

2.9. Implementation of measures that contribute to the acceleration of the turnover of funds in settlements.

2.10. Together with departments and services of the association:

consideration of claims and sanctions filed by buyers and customers, and development of proposals to eliminate the shortcomings that cause these claims;

Claims (together with the Legal Department) and enforcement of sanctions against buyers, suppliers and customers; taking measures (together with the legal department and the main accounting department) for the timely and complete collection of receivables from buyers, tenants and other debtors.

2.11. Implementation of the most appropriate forms of settlements with buyers and suppliers that contribute to the timeliness of payments, and ensuring compliance with the rules for conducting these settlements.

2.12. Receipt, storage, operational accounting and issuance of cash, securities and forms strict accountability in accordance with the Regulations on the conduct of cash transactions.

2.13. Compliance with the limit of the balance of cash in the cash desks of the enterprise established by the relevant bank and ensuring the complete safety of banknotes.

3. In the field of control and analytical work

3.1. Implementation of control:

for the implementation of indicators of financial, cash and credit plans, as well as plans for profit and profitability;

for the state of shipment and sale of products;

for the use for the intended purpose of own and borrowed working capital in general for the association and for individual structural divisions, for which the heads of the relevant enterprises of the enterprise are responsible for compliance with the working capital standards;

to prevent the diversion by departments, services and workshops of working capital of the main activity for capital construction and overhaul;

for the timely consideration by the relevant departments, services and workshops of buyers' claims and reasons for refusing to pay payment requirements for shipped products and services rendered; for compliance with departments, services and workshops deadlines to verify the acceptance of payment claims of suppliers, contractors and other organizations and their timely and proper execution in appropriate cases, complete or partial refusals to pay payment claims in strict accordance with the bank instruction;

for the implementation of plans and estimates of income and expenses of housing and communal services and other similar services;

for compliance with the targeted use of non-centralized sources of financing for the costs of non-centralized state capital investments provided for in the plan;

for receiving cash in banking institutions for the payment of wages and other expenses strictly within the amounts due, determined on the basis of

established rules and cash plans approved by the enterprises of the association, and for the observance of cash discipline.

On all issues related to the implementation of these functions, the financial department makes its proposals to the management of the enterprise.

3.2. Together with the main accounting department and the capital construction department, check:

compliance of the cost of equipment under orders and concluded contracts with appropriations for these purposes, provided for by centralized and non-centralized sources of financing capital investments;

the correctness of the preparation, execution and approval of estimates, calculations of the payback of capital investments for the introduction of new technology and the expansion of the production of consumer goods, carried out at the expense of the production development fund and bank loans, as well as estimates for the expenditure of incentive funds and other funds for special purposes.

3.3. Implementation of a systematic analysis of accounting, statistical and operational reporting on issues related to the implementation of financial, cash and credit plans, compliance with financial and payment discipline; forecasting the results of economic and financial activities; improving the use of fixed assets and working capital; identification and mobilization of intra-industrial reserves and additional sources of financing.

3.4. Participation in the organization of work on the analysis of the production and economic activities of the association and the determination of the impact of this activity on financial performance. .

3.5. Participation in the consideration of cost estimates for production, for the development of new equipment, for future expenses, for the maintenance of administrative apparatus, for the maintenance of buildings, structures, clubs, parks, children's camps transferred to the free use of trade union organizations.

3.6. Participation, together with the planning and economic department, in the development and consideration of draft prices approved in accordance with the current legislation for new products manufactured by the enterprise, as well as tariffs for works and services performed by the enterprise.

3.7. Participation in the conclusion of business contracts and acceptance of financial conditions.

3.8. Participation in the work to improve the organization and planning of working capital and in the implementation of measures aimed at accelerating the turnover of working capital of the enterprise.

3.9. Participation in the development and implementation of measures to improve the internal cost accounting in structural divisions enterprises.

V. The relationship of the financial department with other departments of the enterprise

1. With the planning and economic department and the main accounting department.

Receives: production plan according to the nomenclature for the year, quarter, month; production plan according to the nomenclature and volume of marketable products by workshops.

Represents: financial plan; reports on the implementation of the financial plan; copies of assignments to workshops and departments to reduce working capital stocks; daily information on the implementation of the implementation plan by the shops and the enterprise as a whole.

2. With logistics departments, external cooperation

Receives: conclusion on claims made by suppliers; reporting data on the movement of materials and their balances at the end of the month.

Represents: invoices for acceptance; information about materials in transit; information about unpaid invoices, indicating the reasons.

3. With technical departments

Receives: estimates and financial calculations for financing capital investments at the expense of bank loans for the introduction of new technology, for expanding the production of consumer goods; cost estimates approved by the management of the enterprise for research, development and other work and calculations of their effectiveness.

Represents: a plan for financing research and development work on the basis of approved estimates, as well as providing the necessary funds for organizational and technical measures; correctly compiled, executed and approved in the prescribed manner, estimated and estimated financial calculations for the costs of introducing new equipment, estimates for spending funds from special funds and special-purpose funds, checked together with the main accounting department.

4. With capital construction department

Receives: the planned volume, the structure of capital investments, the balance of material assets and the state of settlements in capital construction.

Represents: a plan for financing capital investments prepared jointly with the department of capital construction for state plan taking into account the mobilization of internal resources in construction.

5. With sales department

Represents: notification of bank institutions about letters of credit issued by buyers and customers, information about buyers who have delayed payment of invoices or refused to accept them, as well as notifications about the application of banking sanctions to buyers and customers.

6. With legal department

Receives: the decision of the management on the transfer of funds based on the results of consideration of claims and lawsuits; notes on bank documents on the receipt of funds on considered and satisfied claims and claims; instructions for the listed state fees on arbitration claims.

Represents: completed claim materials and executed for filing claims with arbitration bodies; conclusions on claims and lawsuits in connection with refusals to pay bills, errors in their presentation, etc.; certificates on the transfer of funds in connection with the consideration of claims and arbitration claims; documents on the transfer of state duty; conclusions on contracts to establish the form of payment.

1. Require the divisions of the enterprise to submit materials (data from the analysis of economic activities of accounting, statistical and operational accounting, etc.) necessary for the implementation of work that is within the competence of the financial department.

2. Control the financial activities of the enterprise's divisions and give their leaders recommendations on the organization and conduct of financial work.

3. Based on the results of economic activity, make proposals to the management of the enterprise on the application of sanctions and incentives in relation to individual employees and divisions of the enterprise.

By authorization of the management of the enterprise, manage financial resources and sign (with the first signature) monetary, payment, settlement, credit and other financial documents, in compliance with current legislation, rules of contracts, instructions, as well as approved plans and estimates.

5. Represent the company in financial, credit and other organizations on financial matters.

6. Approval of all documents related to the financial activities of the enterprise (plans, estimates, reports, contracts, orders, orders, etc.).

7. Instructions of the financial department, within the limits of the functions provided for by this Regulation, are mandatory for management and execution by the divisions of the enterprise.

VII. Responsibility

1. Full responsibility for the quality and timeliness of the implementation of the tasks and functions assigned by this Regulation to the department is borne by the head of the department.

2. The degree of responsibility of other employees is established by job descriptions.

|

(head of structural |

||||||

|

(signature) |

(surname, initials) |

|||||

|

divisions) |

00.00.0000 |

|||||

|

AGREED |

||||||

|

(official with whom |

||||||

|

Regulation is agreed) |

||||||

|

(signature) |

(surname, initials) |

|||||

|

00.00.0000 |

||||||

|

Head of the legal department |

||||||

|

(signature) |

(surname, initials) |

|||||

|

00.00.0000 |

||||||